Cotton

Market situation

The world cotton market experienced dramatic developments in the first half of the 2015 marketing year (see glossary for a definition of marketing year) caused by an acute drop in production – about 9% – in major producing countries. Worldwide cotton production has not declined this much since 2008. This unexpected drop in production led to releases of stocks; however, total world stocks still remain at a very high level (20 Mt, 5% down from 2014).

Production fell in almost all major cotton producing countries led by Pakistan, the United States, and China, which experienced declines of 5%, 19% and 17%, respectively. Adverse weather, lower global world market demand and policy uncertainty all contributed to the sharp decline. The decreased synthetic fibre prices driven by substantially lower oil prices placed huge competitive pressures on world cotton markets. Nonetheless, cotton mill consumption is estimated to increase by 1% from 2014 to around 24.3 million tonnes (Mt) in the 2015 marketing year. Mill consumption estimates in China and India remained stable at 7.7 Mt and 5.3 Mt respectively, Pakistan experienced over 2% and Bangladesh over 4% growth while Viet Nam picked up 6% as Chinese direct investment in mills of the latter two countries continues to increase.

Global cotton imports declined for the third consecutive season, falling 2% from 2014, to 75 Mt. Increases in imports by Indonesia, Turkey and Viet Nam were insufficient to offset the 12% decline in China’s import demand from 2014, as their new cotton support policy narrowed the price gap between domestic and imported cotton. With lower output, US exports are estimated to fall to 2.2 Mt, about 11% below the previous year. India’s exports however increased slightly.

Projection highlights

Although the world cotton price is under pressure from substantial high stock levels and fierce competition from synthetic fibres, cotton prices are expected to be relatively stable in nominal terms after an anticipated further drop in 2016. During 2016-25, relative stability is expected as government support policies stabilise markets in major cotton producing countries. However, world cotton prices are expected to be lower than the average in 2013-15 in both real and nominal terms.

World production is expected to grow at slower pace than consumption during the first few years of the outlook period, reflecting the anticipated lower price level resulting from the large global stocks that accumulated between 2010 and 2014. The stock-to-use ratio is expected to be over 40% in 2025, which is at the high-end of historical levels but well below the historical high of 87% in 2014. World cotton area should be stable for the first five years but it is projected to grow from 2020 onwards. Yields rise around the world and global average yield grows slowly as production switches from relatively high yielding countries, notably China, to relatively low-yielding ones in South Asia.

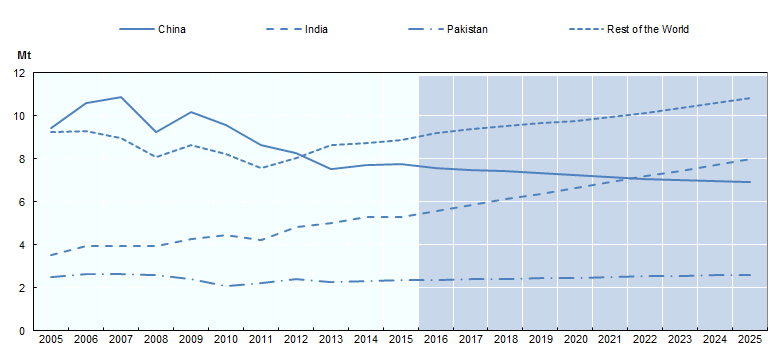

World cotton use is expected to grow at 1.5% p.a. as a result of economic and population growth, reaching 28.3 Mt. Consumption in China is expected to fall to 6.9 Mt following the downward trend started in 2010, while India becomes the world’s largest country for cotton mill consumption (8 Mt) in 2025. Higher cotton mill consumption by 2025 is also foreseen for Bangladesh, Pakistan, Turkey, Indonesia and Viet Nam.

Figure 3.8. Cotton consumption by region

Source: OECD/FAO (2016), “OECD-FAO Agricultural Outlook”, OECD Agriculture statistics (database), http://dx.doi.org/10.1787/agr-data-en.

It is expected that the growth in global cotton trade will be slower compared to previous years, especially 2011-13, when growth was driven by surging Chinese imports. To obtain value-added from mills, a shift to trading cotton yarn and fabrics rather than raw cotton has emerged over the past few years, which is expected to continue. Nonetheless, by 2025 global raw cotton trade will reach 8.7 Mt, nearly 7% higher than the average during 2013-15. The United States retains its position as the world’s largest exporter, accounting for 28% of world trade. Exports from Brazil are expected to almost double from 0.7 Mt to 1.5 Mt, making it the world’s second largest cotton exporter. With higher production, Australia is expected to increase cotton exports to 1.1 Mt, over 70% more than in the base period. Cotton producing countries in Sub-Saharan Africa, as a whole, will increase their exports to reach 1.4 Mt by 2025. On the import side, China is expected to import 1.6 Mt in 2025 and retains barely its position as the world’s largest import market. Its dominant role in the world cotton market will be significantly challenged as other importing countries emerge. It is projected that by 2025, Bangladesh, Indonesia and Viet Nam will each import more than 1 Mt.

While continuing increases in farm labour costs and competition for resources with other agricultural crops place significant constraints on growth in global cotton production, higher productivity driven by technological progress, including greater adoption of bio-tech cotton, creates substantial potential for cotton production to expand in the next decade. While the medium-term prospects are for sustained growth, there may be potential short-term uncertainties in the current Outlook which may result in short-term volatilities in demand, supply and prices. A sudden slow-down in global economy, a sharp drop in global textiles and clothing trade, quality and price competition from synthetic fibres and changes in government policies are important factors that can affect the cotton market. The unprecedented high stock level is a key driver of the world cotton price.

» Access the cotton chapter and all graphs on the OECD iLibrary