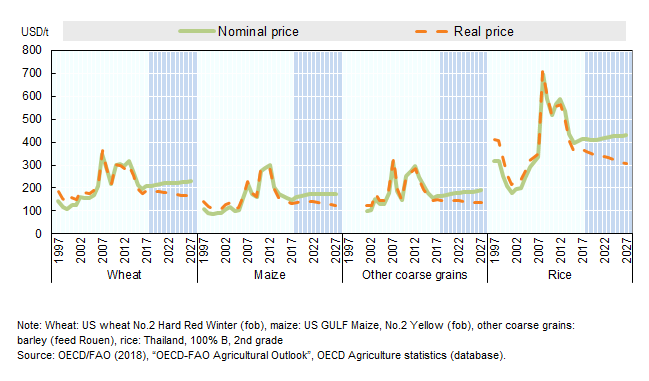

Biofuels

Market situation in 2017

Crude oil prices increased by 25% in nominal terms in 2017, but remained weak at USD 54.7 per barrel on average over the course of the year. The evolution of biofuel and biofuel feedstock prices was contrasting. Maize and ethanol prices declined by 5% and 2.3% respectively, while vegetable oil and biodiesel prices increased by 1.8% and 8% respectively. The biofuel-to-biofuel feedstock price ratios increased slightly but remained below their average values over the previous decade.

Policy decisions were globally favourable to biofuels in 2017 with developments such as mandate increases and differential taxation systems or subsidies enacted or announced in several countries. Demand for biofuels was sustained by bioenergy obligatory blending and by important demand for transportation fuels due to continued low energy prices. Unfavourable price ratios of biofuels to conventional fuels resulted in limited demand for non-mandated use of biofuels.

Global caloric sweetener consumption

Projections (2018-2027)

International crude oil prices are expected to increase by 40% in nominal terms over the baseline period. This should lower demand for gasoline and diesel fuels, especially in developed countries. Biofuel prices, similar to biofuel feedstock prices, should trend slightly upward but at a slower pace than energy prices. Influenced by developments on the vegetable oil markets, biodiesel prices are expected to increase at a slower pace than ethanol prices in nominal terms. Global biodiesel and ethanol prices should decrease respectively by 18% and 4% in real terms over the next decade. The evolution of ethanol and biodiesel markets over the baseline period is expected to continue to be driven by policies. Biofuel policies are subject to uncertainty. Projections presented for biofuel markets in this Outlook assume a continuation of current policies over the next ten years, although some general policy targets will not be met owing to the absence of the necessary policy instruments to achieve them.

For the United States, all mandates are assumed to remain at their announced levels for 2018 except the cellulosic mandate. The latter is assumed to more than double over the projection period, but to reach only 4.5% of the level specified in the 2007 Energy Independence and Security Act (EISA) by 2027. The ethanol blend wall is set to increase to 11.3% by 2027. This Outlook thus assumes a limited development of mid-blends of ethanol. In addition, biodiesel use is assumed to remain above the biodiesel mandate in the early years of the outlook period to meet part of the advanced mandate (see Figure above).

The use of biofuels in the European Union is assumed to be governed by the 2009 Renewable Energy (RED) and Fuel Quality Directives and the 2015 ILUC Directive, as well as by national legislations. The proportion of total transportation energy accounted for by biofuels, including double counting for waste- and residue-based biofuels, is expected to reach 5.9% by 2020 and to decrease to 5.8% by 2027. The remainder of the 10% RED target should be met from other renewable energy sources. This Outlook does not take into account the European Parliament’s proposal agreed to on 17 January 2018 to reach 12% renewable energy in transport by 2030. This proposal also places other restrictions on the use of biofuels based on food and feed feedstocks described below.

It is assumed that the Brazilian taxation system will remain favourable to hydrous ethanol rather than to gasohol, which corresponds to the mandatory mix of 27% ethanol with gasoline. The Brazilian ethanol demand is expected to increase by 5.4 bln L over the outlook period, and the country’s biodiesel mandate should reach 10% by 2020, leading to an increase in biodiesel production of more than 40% over the next ten years. The RenovaBio programme was signed in January 2018 and should be implemented in the course of 2019. The programme targets a fuel ethanol share in the fuels matrix of 55% by 2030, compared to the 50% share assumed in this Outlook. In Argentina, it is assumed that the 10% blending mandate for biodiesel and 12% mandate for ethanol will be fulfilled by 2020. The primary focus of Argentinean biodiesel production will probably be domestic, although some biodiesel trade is expected in the early years of the projection period, principally to the European Union as trade barriers will limit US import demand.

In September 2017, the Chinese government announced a new nationwide ethanol mandate that expands the mandatory use of E10 fuel from 11 trial provinces to the entire country by 2020. Mechanisms for implementation have not been announced yet and thus the announcement is not taken into account in this Outlook. Thailand is expected to expand its domestic ethanol production by 1.2 bln L by 2027, becoming a significant player on biofuel markets. The Thai Government plan to increase use of biofuels entails a differential taxation and subsidy system that are favourable to higher blends of ethanol in gasoline.

The Indian government should continue to support the production of ethanol from molasses. It is assumed, however, that the observed blending share of ethanol in gasoline will remain lower than the 5% mandate and will decline over the projection period. The Indonesian government has a 20% biodiesel blending mandate; however this Outlook assumes this mandate will not be fulfilled as the development of biodiesel is related to the potential attribution of subsidies to biodiesel producers who depend on vegetable oil exports.

Given these policy assumptions as well as the IEA assumptions concerning future diesel and gasoline demand across the world, global ethanol production should expand from 120 bln L in 2017 to 131 bln L by 2027, while global biodiesel production should increase from 36 bln L in 2017 to 39 bln L by 2027. By 2027, 55% of global ethanol production should be based on maize and 26% on sugarcane. In 2027, about 20% of global biodiesel production should be based on waste vegetable oils. Advanced biofuels based on residues are not expected to take off over the projection period due to lack of investment in research and development.

Trade disputes related to biofuels have had a major impact on the recent evolution of biofuel trade. Following a 2018 WTO ruling, Argentina and Indonesia can again export biodiesel with lower duties to the European Union. However, anti-dumping duties have recently been set up in the United States against these countries’ biodiesel, and which may once again be challenged at the WTO. As such, this Outlook assumes biofuel trade will remain limited. Potential ethanol exporters are the United States, as the blend wall limits further increases in domestic demand, and Brazil. Brazilian ethanol exports are, however, not expected to increase as US ethanol will likely remain cheaper over the outlook period. On the biodiesel side, Argentina will likely be the major player, but with limited import demand.

» The full chapter is available here.

Related Documents